What Does Foreclosure Do to Your Credit

August 22, 2018 A foreclosure is viewed quite negatively by lenders. It is important to research the exact consequences of a foreclosure on your credit.

A foreclosure is viewed quite negatively by lenders. It is important to research the exact consequences of a foreclosure on your credit.

So, what is a credit score? We know that a credit score is the barometer via which lenders gauge your credit worthiness. But, what are the various factors that impact your credit score? Does your credit score affect your mortgage rate? I also discuss the consequences of a foreclosure on your credit score. What are the various ways of buying a home after foreclosure? And finally, I wrap up by providing some common sense ways to bump up your credit score. Read on to discover some interesting insights that will help address some common pain points.

Defining Credit Score – How Credit Scores affect mortgage rates

Your credit score is a gauge of your financial health. A credit score is a numerical expression which predicts the likelihood of you not meeting your financial obligations. This score is calculated based on five important parameters:

- Payment History

- Debt Usage

- Length of credit

- Account Mix

- Credit Inquiries

It is interesting to note that payment history contributes 35% to your credit score – more of a reason to pay your mortgage bills on time.

The FICO score is the most popular score. FICO is the credit bureau that has developed this popular credit score. Experian, Transunion and Equifax are the other prominent credit bureaus.

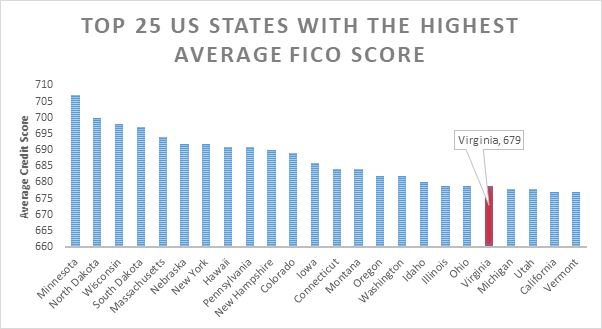

In fact, real estate investors can benefit from looking at average FICO scores for different US states. Please find below the top 25 states with the highest FICO scores (Virginia with a respectable credit score of 679 is in this list). States with higher FICO scores will have a lower foreclosure rate compared to states with a lower FICO score. Minnesota scored the highest with a FICO score of 707. North Dakota and Wisconsin were at number 2 and 3 respectively.

National Equivalency Score and Vantage Score are some other credit scores that you are likely to refer. Generally a FICO score of 720 and above is considered to be ideal. However, you can avail a mortgage with a FICO score of as less as 500. Generally speaking, a higher score means more favorable lending terms.

A low credit score means a higher risk of default. For instance, let us say that a bank is offering mortgage lending rates ranging from 4% to 6%. Someone with a credit score of 600 is likely to be offered a lending rate which is closer to 6%. Similarly, someone with an excellent credit score (720 plus) might be offered closer to 4%.

Consequences of a Foreclosure on Your Credit Score

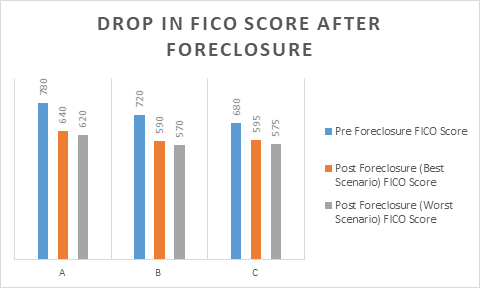

Let us deep dive into the consequences of a foreclosure on your credit score. It is interesting to note that a higher credit score will witness a greater fall as a result of a foreclosure.

Let us consider three scenarios – A, B and C. Scenario A has a starting FICO Score of 780. For Scenario B it is 720 and for Scenario C it is 680. So, if your credit score is 780, a property foreclosure can mean a drop of up to 160 points. A 720 credit score means a drop of 130 to 170 points.

A 680 credit score will see a drop of 85 to 100 points due a foreclosure.

The effect of a foreclosure on your credit report is pretty drastic – a foreclosure remains on your credit report for 7 years. However, if you observe prudent financial practices, your FICO score might start seeing an upward trend in 2 years.

Buying a home after foreclosure

Have you recently gone through a foreclosure? Wondering if you will ever be able to buy a house again? We have already discussed the consequences of a foreclosure on your credit. You know that the impact is pretty drastic. Post foreclosure, there are two key measure to help you improve your credit score – patience and financial discipline.

Note that FHA loans have some of the most lenient lending practices. In fact, you might be able to avail a FHA loan with a FICO score of as low as 500! And for folks who wish to take out a mortgage after foreclosure, FHA loans are your best bet. You can consider for a FHA loan 3 years after your foreclosure.

Availing a loan from Fannie Mae or Freddie Mae will take you longer – 7 years. However, there are some ways via which you can avail a Fannie Mae/Freddie Mae loan faster. For instance, if you plan on using the new property as your personal residence, you do stand a slim chance (You cannot use this loan to purchase an investment property)

Most conventional lenders are not as lenient as FHA or Freddie Mae/Fannie Mae. The waiting period might be longer. Or, they might ask you for a much larger down payment. Or, maybe the interest rate will be really high.

Conclusion

There is no denying the adverse impact of a foreclosure on your credit. However, understanding the science behind credit scores helps you understand how you can recover from it. Payment history is the biggest contributor to your credit score. And paying your bills on time is the biggest factor that will help you bump up your score over time. Keep on monitoring your credit report for any inaccuracies. And avoid taking out any new loans. These common sense measures will help you increase your credit worthiness and hence, get more favorable lending terms.

If you liked what you read, please leave a “Like” or a “Comment” – Your encouragement keeps us going!

Do not hesitate to get IN TOUCH with us with your real estate needs.