How much house can I afford?

June 6, 2018

Discussing Home Affordability Index and Mortgage Affordability Calculators

In this blog post, I talk about mortgage affordability or housing affordability. I start off by talking about the housing affordability index. Real estate investors can gauge investing climate by studying this index. Next I provide tips for using a mortgage affordability calculator, and provide insights into their results. Can you really base your investment decision off these results? And finally, I wrap up by discussing some Pro Tips which would help you avoid some common mistakes that home buyers makers. Read on.

Understanding Mortgage Affordability

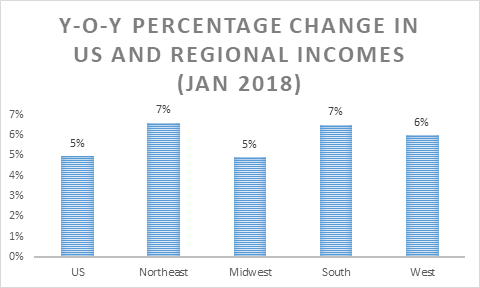

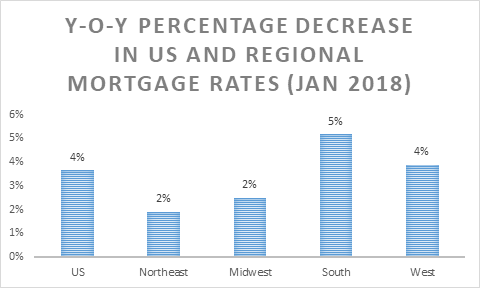

On a macro level, mortgage affordability can be gauged by following the housing affordability index. As per January 2018 Housing data, housing affordability index is up MOM but down YOY. Housing affordability measures the ease with which a typical US family is able to meet its loan obligations. This index is dependent on factors such as the median prices of single family homes and current mortgage rates. So, while incomes increased,

YOY Mortgage rates decreased,

And yet, housing affordability declined by 1.1%.

Housing affordability declined from 164.8 in January 2017 to 163 in January 2018. So, in spite of decreasing mortgage rates, houses became less affordable. It is interesting to note that Northeast showed a 7% increase in income as compared to a national average of 5% (Alexandria, VA remains a good place to invest).

Mortgage Affordability Calculator

Now that we have looked at mortgage affordability from a macro level, let us get into the nitty gritty of it. Let us look at mortgage affordability or home affordability from a layman’s perspective. “How much home can I afford?” is a popular query among home owners. Using a mortgage affordability calculator can help you answer this question. Affordability is a function of:

- Household income

- Monthly Expenses and Debts – Credit card bills, groceries, student loans etc.

- Down Payment and Closing Expenses – You can use your savings to fund these. Closing expenses are generally 3%-6% of house cost

Lenders generally use the 36% rule to determine the amount of mortgage that you can afford to pay. So, if you have an income of $100,000, according to this rule, you can afford an annual mortgage payments of $36,000. If your Debt to income ratio (DTI) is greater than 36%, you will find it difficult to avail a conventional mortgage. FHA loans are the most lenient – they permit a DTI of 43%. Permissible DTI for VA or USDA loans is 43%.

Apart from the above, you also need to set aside a “Rainy Day Fund” or an “Emergency Fund” which you can use in the event of unforeseen circumstances. While calculating your mortgage affordability, there are some significant costs that home buyers often tend to overlook. Some of them are:

- Property Taxes

- Mortgage Insurance

- Homeowner’s Insurance

- Closing Costs

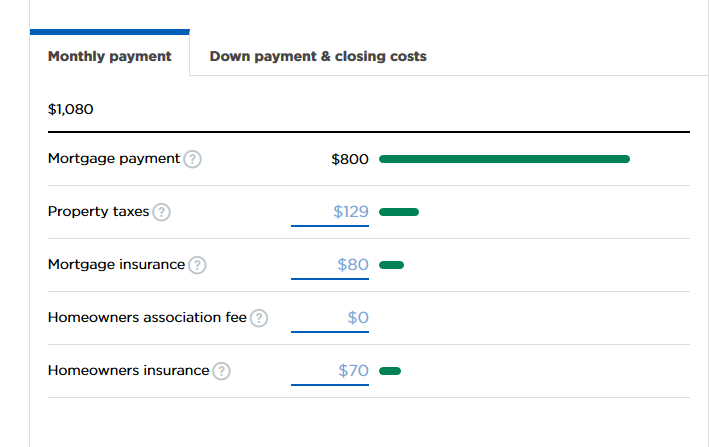

For instance, I came across this great mortgage affordability calculator by Nerd Wallet aptly titled, “How much Home can I afford?” I calculated home affordability for a home in Richmond, VA. I assumed a loan term of 30 years, an annual income of $100,000 and monthly debt payments of $2,000. This data was calculated for a homeowner with a credit history of 720 and above (4.6% interest rate). And the calculator threw out some interesting numbers:

Property taxes, Mortgage Insurance and Homeowner’s Insurance accounted for nearly 26% of the total monthly mortgage. The biggest component was Property taxes. Property taxes vary quite a bit depending on where you stay. Generally speaking, property taxes are higher in larger cities. Property tax in Richmond, VA was $1.2 for every $100. While taxes in Ashland, Virginia were just $0.09 for every $100!

PRO Tips for Home Buyers

- Owning a home is a huge responsibility. You will have to constantly spend after repairs and devote time to yard work. If you value your flexibility, you are better off renting.

- If you are unable to pay 20% down, you might have to cough up a higher interest rate.

- Using a Mortgage affordability calculator is a great first step. However you cannot make your final investing decision based on its results. You need to dive deep and factor in all future expenses and uncover any hidden costs.

- While FHA loans seem really lucrative since they are available with just 3% down payment. Before rushing in, do factor in the cost of Primate Mortgage Insurance (PMI).

- Carefully go through all fine print before you sign on the dotted line. Make sure that there are no hidden costs.

- Once you receive an official loan estimate, you MUST shop around for a better deal. Lowering the interest rate by just half a percent will save you a lot of money.

- Make sure that you have enough set aside for events like child birth or illness.

- If you are buying a house on resale, make sure that you go for a through home inspection

- Avail the help of a good real estate broker who can guide you through the entire process.

Conclusion

Home affordability is a complex subject. However it is crucial for home investors and home owners to dive deep into this topic. Home affordability index is a great way of gauging and comparing regional real estate investing conditions to national averages. While, home owners shall really benefit by using a mortgage affordability calculator in the initial stages of the home buying process. However, a word of caution here. Do NOT base your final decision off these results. You need to carefully read the fine print and ensure that there are no hidden costs before making your final purchase.