How Property Tax Deductions are Making Home Ownership More Affordable

August 29, 2018 Feeling burdened by your mortgage payments? You will be heartened to know that Uncle Sam is doing his bit to share your pain. Property tax deductions go a long way in saving you moolah and making home ownership more affordable. Did you know that your property tax deductions do not remain constant across your loan term? What are some particulars of the Republican Tax Bill of 2017 that majorly affect homeowners? We also discuss how property tax deductions have a bearing on the whole renting vs. buying argument. And we also share a detailed analysis showing why property tax deductions make home ownership particularly attractive to those in the higher tax bracket. Read on to get insights into these important points.

Feeling burdened by your mortgage payments? You will be heartened to know that Uncle Sam is doing his bit to share your pain. Property tax deductions go a long way in saving you moolah and making home ownership more affordable. Did you know that your property tax deductions do not remain constant across your loan term? What are some particulars of the Republican Tax Bill of 2017 that majorly affect homeowners? We also discuss how property tax deductions have a bearing on the whole renting vs. buying argument. And we also share a detailed analysis showing why property tax deductions make home ownership particularly attractive to those in the higher tax bracket. Read on to get insights into these important points.

Understanding how Property Tax Deductions Vary across the Entire Loan Cycle

Your monthly mortgage payment includes two components – the principal payment and the interest payment. You can claim property tax deductions on your interest payments. Note that while your mortgage payment remains constant every month, the interest and principal components are not equal. At the beginning of your loan term cycle, a greater portion of your monthly mortgage will be towards your interest cost. So, in the initial years the property tax deduction that you can claim will be greater. Contribution towards interest will gradually reduce as you progress through your loan term. Check out our article on Loan Amortization in order to understand how this works.

The Republican Tax Bill introduced in December 2017 lowered the cap from mortgage interest deduction from $1 million to $750,000. This Bill also capped annual mortgage deductions at $10,000 (this includes property, state and local taxes). As of 2017, the real estate tax for the city of Virginia was $1.13 for every $100. Under this Bill, you can avail $250,000 capital gains exclusion as a single filer. Joint filers can avail exclusion of $500,000. The only catch is that you must have stayed in the house for 2 of the last five years.

Renting vs. Buying – How Property Tax Deductions Make Home Buying more Attractive

So, how can buying a house help you claim more in property tax deductions? If you are landlord renting out your home in Alexandria, VA, your rental income will be taxed. Similarly, if you are the renter, you cannot claim deductions on the rent that you pay. However, if you are a homeowner, there are many property tax deductions you can claim to make your home purchase more affordable.

The theory of “imputed rent” is particularly interesting, albeit slightly confusing. Let us presume a renter who is paying $1,000 rent per month. So, your landlord is generating a rental income on which he is paying tax. Now, if you buy out this property, effectively you become your own landlord. (Since you paying rent to yourself) And this is what the taxman defines as “imputed rent”. US citizens will be surprised to know that countries like Netherlands tax home owners for staying in their own houses. Luckily, there are no such taxes in United States.

Can you Claim Mortgage Insurance Deductions?

If you paid less than 20% down, it is likely that you will be paying Private Mortgage Insurance (PMI). PMI can contribute substantially towards your monthly mortgage. The Tax Relief and Health Care Act of 2006 allowed for mortgage insurance deductions till 2016. Unfortunately, only a 1 year extension was provided, and you cannot claim insurance deduction currently. However, all hope is certainly is not lost. Congress might renew mortgage insurance deductions and again provide some much needed relief to homeowners.

Property Tax Deductions make Home Ownership More Attractive for Folks in the Higher Tax Bracket

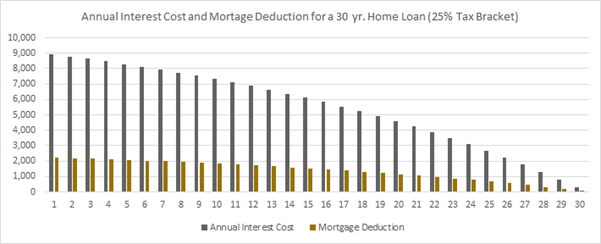

Remember, if you are in the lower tax bracket, you will not be able to save much. It is simple – You can’t save if you don’t owe much in taxes. So, if you are in a higher tax bracket, you certainly have more of a reason to buy a house and save your taxes. Let us consider that you take a $200,000 mortgage paying 4.5% interest rate. And let us presume a 30 year loan term. Using one of the many loan calculators, it is easy to calculate your total interest cost over 30 years – $164,813. Interest burden for first year will be $8,934. Thus in the first year itself, someone falling in the 25% tax bracket can claim deductions of $2,234. Cumulative tax deductions at the end of 30 years will be $41,203. Not a small amount by any means. Check out the following graph which shows how your interest payments and mortgage deductions vary over the entire loan term of 30 years.

Some Other Property Tax Deductions You can Claim

If you are paying points, you can claim a deduction on these as well. So, what are points? Borrowers pay points in order to lower their mortgage rates. 1 point translate to 1% of the loan value. So, 1 point on $200,000 home loan means $2,000.

Folks operating their small business from a home office have another reason to rejoice. They can claim deductions on expenses such as electricity and water. So, if you have a 3000 square foot home and your home office occupies 150 square feet, you can claim deductions totaling to 5% of total expenses.

Conclusion

Property tax deductions is a vast and complicated field that requires detailed analysis. Be mindful of all the tax deductions that you can claim. Every home owner has a different financial situation – and hence, tax deductions vary from a case to case basis.

Analyze ways to increase your property tax deductions. Will purchasing points work out to your benefit? Can you claim deductions for your home office? Are you factoring in all state and local taxes? These are the questions that you should be asking before you sign on the dotted line.

If you liked what you read, please leave a “Like” or a “Comment” – Your encouragement keeps us going!

Do not hesitate to get IN TOUCH with us with your real estate needs.