How to buy a house with no money down – All you Need to Know About FHA loans, HUD homes and USDA homes

August 8, 2018 It is a common misconception that you need to pay 20% down in order to purchase a house. Nothing could be farther from the truth. In this blog post I talk about some real estate investing hacks which will help you buy a house with no money down. How can you purchase a FHA home with no money down? Can HUD homes be purchased with no money down? What about USDA loans? Are they an attractive option? Read on to find answers to this commonly asked questions.

It is a common misconception that you need to pay 20% down in order to purchase a house. Nothing could be farther from the truth. In this blog post I talk about some real estate investing hacks which will help you buy a house with no money down. How can you purchase a FHA home with no money down? Can HUD homes be purchased with no money down? What about USDA loans? Are they an attractive option? Read on to find answers to this commonly asked questions.

Using a FHA Loan for buying a house with no money down

Purchasing a FHA home is a great alternative if you wish to purchase a house with no down payment. FHA has some of the most lenient lending practices in the country. Typically, a FHA loan requires you to just put 3.5% money down. And, if your credit score is really, you need not despair. You can avail a FHA loan even with a score of 500. (You will have to furnish a 10% down payment in this case)

Wondering if you can get a FHA loan with no down payment? Yes, there are some great hacks for doing so. For instance, you can ask your relatives to give you a gift to cover your down payment. Though, you need your relative to certify that the money does not need to be repaid. You can also have a FHA approved charity, non-profit or even your employer gift you the down payment amount.

Cannot arrange a gift to fund your loan down payment? You can also take advantage of the Down Payment Assistance Program. This program permits the borrower to arrange secondary financing from a third entity. This entity should be party that has not financial interests in the property sale.

Pro Tip – HUD Homes can fetch you some great bargains!

HUD homes are the ones that were initially purchased through a FHA loan. We talked about the lenient qualifying requirements for a HUD home earlier. Due to these lenient lending practices, quite a large percentage of these houses tend to foreclose. And these are returned back to the FHA. These are available at some great bargains. You can purchase a HUD home using a FHA loan and hence, with no down payment using one of the hacks we talked about earlier.

How to buy a house with no money down using a USDA loan

Prefer the country life over the hustle bustle of the city? Then you would like to know about the housing market’s best known secret – USDA housing. Purchasing a USDA (United States Department of Agriculture Rural Development) house is a great option for those looking to make their purchase with no down payment or minimum down payment.

Their rural development program financed new house purchases/repairs for nearly 127,000 families in United States. Contrary to popular perception, all USDA homes are not situated in rural areas. To qualify for a USDA loan, you need to be within USDA income limits.

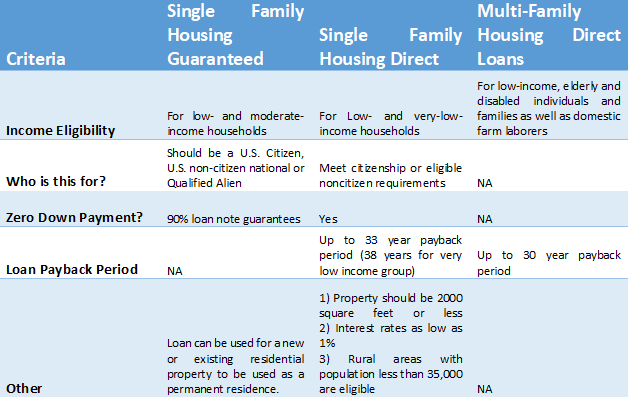

USDA loans can be subdivided into three main categories:

- Guaranteed loans: As the name suggests, the USDA guarantees a home loan issued by a lender. The USDA gives a 90% loan note guarantee for their “Single Housing Guaranteed” program.

- Direct Loans: Direct loans are for households with low or very low incomes. Normally this USDA loan has a loan term of 33 years. In rare cases, it can be even extended to 38 years. Under USDA’s “Single Housing Direct” program, you can avail a loan with zero percent down payment.

- Home Improvement Loans: This USDA loan is meant to finance home repairs.

You can find details about all USDA programs here. Let us look at the details of their three main programs:

Are you eligible for a USDA loan?

There is not minimum credit score requirement to qualify for a USDA loan. But having a credit score greater than 640 makes it easier for you to qualify for a USDA loan as you will be routed through an automatic underwriting process. A credit score less than 640 means that you will have to go through a manual underwriting process to determine eligibility.

In order to be eligible for a USDA loan:

- You need to show proof of stable income

- You must use the home as your primary residence

- You must be a US Citizen. (or, furnish proof of your permanent residency)

- Debt to income ratio should be maintained at 41%

You can look up USDA loan income limits here: Single Family Housing Guaranteed, Single Family Housing Direct and Multi-Family Housing Direct.

Using a USDA loan map is a great way of identifying areas eligible for a USDA loan.

Conclusion

You can very well purchase a home with no money down using a FHA loan or a USDA loan. To be eligible for a FHA loan, you need to make sure that your credit score remains above 500 (worst case scenario) and ideally, above 580. Using a cash gift or the down payment assistance program will let you buy a house with no money down.

If you liked what you read, please leave a “Like” or a “Comment” – Your encouragement keeps us going!

Do not hesitate to get IN TOUCH with us with your real estate needs.