Expert Tips for Purchasing a HUD Home

July 4, 2018 There are many bargain hunters who are enamored by the idea of purchasing a HUD foreclosure. HUD home is owned by the Housing Urban and Development Authority. HUD homes are available at extremely attractive market rates, and are often, far below market value. They are 1-4 unit residential properties. HUD homes are homes that were initially purchased with a FHA loan.

There are many bargain hunters who are enamored by the idea of purchasing a HUD foreclosure. HUD home is owned by the Housing Urban and Development Authority. HUD homes are available at extremely attractive market rates, and are often, far below market value. They are 1-4 unit residential properties. HUD homes are homes that were initially purchased with a FHA loan.

In comparison to a conventional loan, it is far easier to quality for a FHA loan. In fact, you can qualify for a FHA loan with a FICO score of 500! Folks with a credit score of 500 will have to furnish a 10% down payment. And if you have a FICO score greater than 580, you can qualify for a HUD foreclosure with just 3.5% down.

Because FHA qualification is so lenient, it is of little surprise that foreclosure rates are higher than industry average. Mortgage Delinquency rate in 2015 for FHA loans was a steep 9%!

If you can avoid some common investing mistakes, you CAN make quite a killing by buying a HUD foreclosure. So, how do you purchase a HUD home? How does an insured HUD home compare to an uninsured HUD home? What are the advantages and disadvantages of purchasing an insured HUD home? What is an owner occupant certification? Do you really need a HUD Form 1? Read on to learn more about HUD homes.

How do I purchase a HUD home?

You can check out the HUD home store. You need to plug in the following information:

- State, County, City and Zip Code

- Price Range

- Number of Bedrooms and Bathrooms

- Buyer Type (eg. Owner Occupant or Investor)

- Property Status

Entering the above information enables you to search the entire HUD database and look up nationwide listings for HUD homes.

Once you have zeroed in on a HUD home of your choice, contact a good broker who can show you these properties.

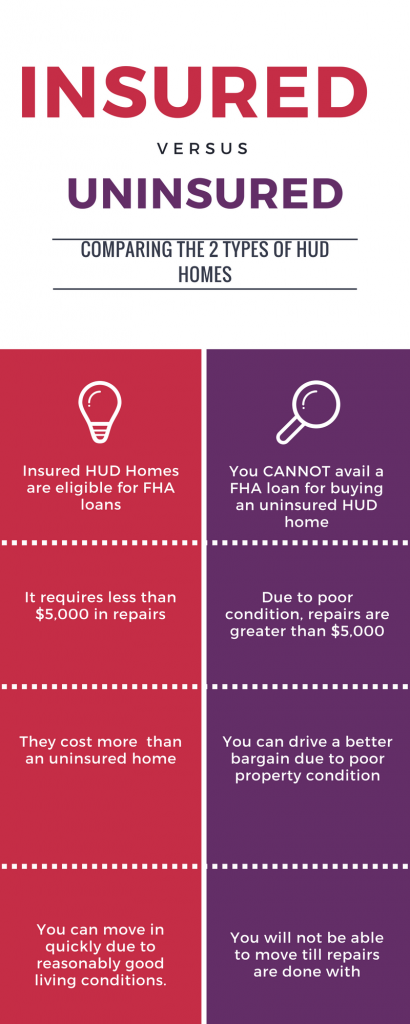

Comparing Insured and Uninsured HUD Homes

There are two main types of HUD homes: Insured (IN) and Uninsured (UI). It is important to be aware to be aware of the pros and cons of each before making a purchase.

Insured HUD Homes are comparatively in better condition than an Uninsured HUD home. An Insured HUD home meets the “Minimum Property Standards” that are defined by the FHA. The main difference is that you cannot avail a FHA 203 (K) loan to purchase an uninsured home. It is extremely important that you hire a good home inspector to accurately estimate repairs cost before making your purchase. Unlike other properties, it is extremely difficult to get your deposit back on a HUD home.

Insured with Escrow Repairs (IE) is another HUD home type. An IE HUD home requires a small amount of repairs (less than $5,000) to meet the Minimum Property Standards as defined by the FHA. Borrowers are eligible for a repair loan. As the name suggests, the loan amount is held in an escrow account.

Do Owner Occupants Have a Better Chance of Buying a HUD Home?

The first preference for a HUD homes is given to an owner occupant rather than an investor. For insured homes, only owner occupants are permitted to bid for a property for the first 15 days. So, how does HUD define an “owner occupant”? HUD has some very clear guidelines. Some important takeaway are:

- For starters, you HAVE to stay in a HUD home for at least 50% of the time.

- Existing home owners take note – You CANNOT use your HUD home as a second home or a vacation home.

- Thinking of buying and quickly selling a HUD home to make a quick buck? Think again. As an owner occupant, you MUST stay in a HUD home for at least one year. You cannot sell or even, rent before that.

HUD takes these guidelines very seriously. I would suggest going over these carefully so that you are not on the wrong side of the law. The penalty for flouting these laws can go as high as $250,000 or 2 years in federal prison.

To prove that you are an owner occupant you will have to sign an owner occupant certification, also known as HUD 9548D. You an access this form from the Department’s website.

For investors, buying an uninsured home is somewhat easier. You can start bidding on the 6th day itself. Because uninsured homes are available at better bargains and not immediately livable, investors stand a better chance of buying an uninsured home as against an insured home.

What is a HUD-1 form? Is it still used?

The HUD-1 form was an important document which listed all incoming and outgoing funds for the buyer and the seller. This settlement statement was developed and used by the US Department of Housing. The Housing Department stopped using this form after October 2015. However, this form is still used in one instance – for reverse mortgages. Reverse mortgage is particularly popular among older folks who wish to borrow against their home equity.

In all other instances, the HUD-1 form has been replaced by a Closing Disclosure.

Conclusion

Buying a HUD home is a complicated and long drawn process. You need to properly evaluate the HUD home market before making a purchase. Investors, lured in by the idea of making some quick money, often end up under-estimating the cost of home repairs. It is prudent to get a thorough home inspection done before purchasing a HUD home. Purchasing a HUD home can understandably feel overwhelming for many home buyers. Do not hesitate to seek out the expert guidance of a knowledgeable real estate broker.

Some patience and wisdom will go a long way in ensuring profitable returns on your HUD home investment.