Understanding the Nuances of Loan Amortization for Smart Financial Decisions

June 20, 2018

Amortization Schedule, Loan Amortization and its Benefits Explained…

Introduction

First time home buyers are understandably overwhelmed by industry jargon commonly used in the mortgage business. One of the terms that is confusing to a lot of folks is “loan amortization” or “mortgage amortization”. So, what is loan amortization? And, why is it important to understand your loan amortization schedule?

In this blog post, I attempt to simplify the concept of loan amortization. I also explain how a loan amortization schedule works. How does amortization result in varying interest and principal payments over the loan term? How can understanding amortization help you evaluate your options? And is re-amortization better than a mortgage re-finance. Read on….

Loan Amortization – What Does It Mean?

Oxford dictionary defines amortization as the process where you “gradually write off the initial cost of (an asset) over a period”.

When you are shopping around for a mortgage, your lender will be quick to quote a monthly mortgage payment. These equal payments are worked out as per the lending rate offered to you. And these are spread out over the duration of the entire loan.

It is interesting to note that you are making a GREATER interest payment in the initial years of your mortgage. While, during the fag end of your loan cycle, a larger proportion of your mortgage payment pays off your loan principal. How so? This is because your loan balance is much higher in the initial years.

Many borrowers treat amortization as an accounting entry, and fail to dive deep into this concept. This is a huge mistake. Understanding amortization can really help you in case you opt for a mortgage refinance (more on this later).

Let us first understand how interest payments and principal payments vary over time.

Learning How a Loan Amortization Schedule Works

Let us consider a traditional, 30 year fixed mortgage for a $100,000 home. I have considered a lending rate of 6%. Using one of the many mortgage calculators, you can easily calculate your monthly mortgage – $599.55.

So, how much interest are you paying at the end of the first month. Using this formula, you can easily calculate the same:

Interest paid at the end of 1st month = Starting Balance * (Rate/12)

So this works out to be,

Interest payment at the end of 1st month = $100,000 *(0.06/12) =$500

Now, it is easy to calculate the amount that goes towards paying off your principal.

Principal paid off at the end of 1st month = Monthly Mortgage – Interest payment at the end of 1st month

And this is,

Principal paid off at the end of 1st month = $599.55 – $500 = $99.55

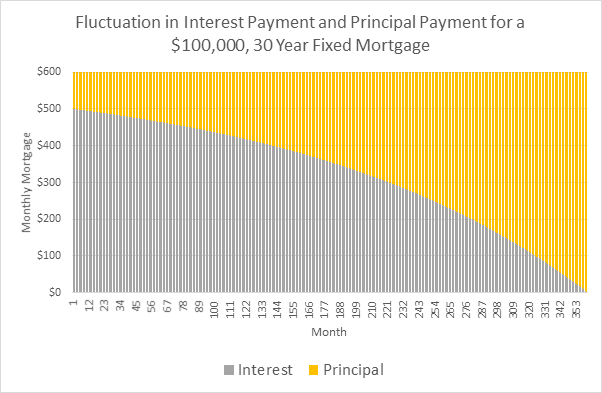

This variation in interest rate is depicted in the following chart:

By the end of 10th year, your interest payment will be $419 and your principal payment will be $180. In the 20th year of your loan term, your interest payment will further reduce to $271. And at the end of your loan cycle, interest will be virtually zero.

As you can easily see from the above chart, your interest payments are decreasing as you progress through your loan term. Initially, your interest payments are greater than your principal payments. Towards the end of your loan cycle, your principal payments are greater.

Thus, as you progress through your loan term, equity in your house increases at a far greater rate.

How Can an Amortization Schedule Help You Evaluate Your Options?

Understanding the Amortization Schedule can provide to be extremely advantageous for you. For instance, you can calculate the total interest that you will end up paying over the loan term. You can also conduct a sensitivity analysis. For instance, do you know how much interest you will end up paying for a $100,000 loan spread over 30 years at 6% rate? $1,15,838!

What if you were able to procure this same loan at 5% interest rate? You will end up saving $22,583 over 30 years. And, what if you availed a 20 year loan at 5% interest rate? You will end up saving a whopping $57,449!

If you wish to pay off your loan earlier, you have two available options– Re-finance or Re-amortization. So, what is the difference between these two?

Clearly, more folks are aware of the first option – refinancing a property. A homeowner typically opts for a refinance when lending terms are more conducive. Refinancing a mortgage will give the homeowner a chance to lower his monthly mortgage. However, refinancing typically attracts a fee. (2-3% of the refinance amount) It might take you some time to recoup this closing cost.

A better approach is re-amortization or recast. Under this option, you are paying off a big chunk of your loan earlier. This allows you to lower your monthly mortgage without paying any fees or closing costs. Of course, you will need cash in hand in order to avail this alternative. Most lenders do not permit a loan recast before 90 days.

Bear in mind that a re-amortization will not lead to a reduction in interest rates. So, if you can, you should opt for both – a refinance first and then a recast. If you are paying an extremely low interest rate, you might be better off investing your excess liquidity elsewhere. Re-amortization is not available for FHA and VA loans.

Conclusion

Amortization is merely not an accounting entry. Homeowners should go the extra mile in order to understand this concept. Understanding how amortization works can help you understand how much your loan is really costing you. Knowing your true financial picture will help you evaluate various financial options such as recast and mortgage refinance. You can make data driven investment decisions which will help you analyze how you can park your funds to extract maximum possible return.